Understanding BSP Digital Payment Rails

General Manager Digital , Digital Insights - Nuni Kulu

An ever-present customer need is the continuous search for a convenient way to make payment. Payments is fast evolving from Cash and Card to Electronic Transfers. The simple exchange of value from one party to another has been refined with technology to make ease of payments convenience the primary experience for consumers. Moving away from traditional payment methods to electronic payment options, the competitive edge comes down to the ability to pay instantly, securely and with ease.

Globally, achieving real-time or near real-time processing of payments is the ultimate goal for big players Visa, MasterCard and even payment processors such as PayPal. The major schemes have invested in payment rails and networks that can move payments globally, swiftly and securely and influence payment standards and compliance practices.

BSP’s electronic payment ecosystem, 20% of the banked market is shifting from Cash- Cheque-Card, to adopting viable and cheaper digital channels electronic transfers, made possible with various payment rails and investment into BSP proprietary network infrastructure over the last 5 years.

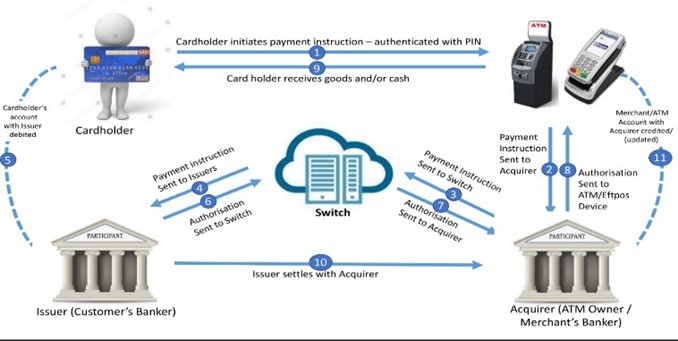

Payment rails are a globally used term describing a network or any form of digital infrastructure that provides the connection between financial institutions to allow for the transfer of money from one individual or business to another. There are three payment networks, which support BSP payments: Major Schemes (Global), BPNG Interchange (National), and the BSP exclusive payment rail.

With the aim to reach a wider customer base of 2.5m account holders across PNG, BSP’s bespoke Consumer to Business (C2B) digital payment solutions, BSP Mobile Merchants and more recently, the BSP Pay Service, BSP’s solution to a Domestic Online Payment Gateway reaffirms the Bank’s strong focus on cheaper alternative payments for both merchants and customers.

In developing an alternative payment rail, and leveraging BSP’s enterprise network, there are new opportunities to allow digital offering to reach all customer segments. For consumers, it allows a customer to make a seamless instant non-card payment to an online merchant or a BSP Mobile merchant. Therein lies opportunity to expand this offering to a card-less transaction via ATMs and EFTPoS as well. A home grown and developed rail, presents a more cost effective payment option to the customer, the merchant and also to the bank.

Automated Clearing House (ACH) volumes have increased as result of the pandemic, as per the National Automated Clearing House Association (NACHA), the stats reveal "the use of the ACH Network to deliver economic assistance to individuals and businesses, as well as an acceleration in the shift from paying by paper cheque to paying electronically".

In similar manner, alternative payments extend to interbank transfers bringing to light the core infrastructure around National Payment Rails, the Retail Electronic Payments Systems (REPS) in PNG is regulated and solely facilitated by the central bank (Bank of PNG).

In similar manner, alternative payments extend to interbank transfers bringing to light the core infrastructure around National Payment Rails, the Retail Electronic Payments Systems (REPS) in PNG is regulated and solely facilitated by the central bank (Bank of PNG).

BSP integration to REPS, as the National payment rails, allows interoperability and seamless payments among financial service providers, and will enable new digital channel payments, not necessarily restricted to cash and cheques and to be facilitated via Eftpos and ATMs transactions.

BSP Acquiring with global schemes Visa, MasterCard, American Express and Union Pay International means from a global market reach and access perspective, cardholders globally can make payments online or in person when visiting PNG for work, tourism and leisure.

In partnership with Visa, Visa Scheme payment network facilitates BSP Visa product customers make payments from their BSP accounts worldwide.

As BSP continues to explore enhanced digital financial solutions, the PNG payments ecosystem has a growing appetite for increased customer adoption and utilization of digital services that processes real time payments and electronic receipts (e-receipts) with a reconciliation timestamp electronically delivered in real time to the receiver of payments.

BSP customers are driving mobile and online payments, particularly with the growing interest, more businesses have boldly set up shop in the online marketplace because of confidence in robust and secure payments channels, that customers are familiar with and growing accustomed to shopping online.

Ultimately, the “ability to pay” takes precedence in our efforts to provide convenient services, and BSP is focused on creating an enabling payment environment that is pragmatic and suitable to our market, as well as developing payment solutions (Alternative/Scheme) to every need of our diversified customer base within urban and rural sectors in PNG and throughout the Pacific region.